PART 1 - Asset Allocation: The Real Driver of Outcomes

- Rajeev Roshan R

- Apr 22

- 15 min read

Updated: May 12

Part 1 of 3 — The Pattern Most Investors Keep Repeating

There is a pattern that plays out, with remarkable consistency, across almost every generation of investors. It does not discriminate by age, income, or education. It catches experienced investors just as often as beginners. And the frustrating part is that while it is happening, it rarely feels like a mistake. It usually feels like good judgment.

The pattern is this: People invest based on what has recently worked, not based on how a portfolio should be structured.

How the Cycle Begins

Suppose small cap funds have had two extraordinary years. The numbers are undeniable. Investors who had money in small caps have seen their portfolios grow in ways that feel almost unreal. Stories are circulating — on social media, at family gatherings, in office conversations — about the returns people have made.

An investor who has been sitting on the sidelines starts to feel uneasy. Not because anything has gone wrong with their own investments, but because of a creeping sense that they are missing out. That the real wealth is being created elsewhere.

So they move money in. They shift allocations away from large caps or debt, feeling that those are slower and less exciting. The recent returns seem to make a very compelling argument.

For a while, this feels intelligent. It feels like staying ahead of the market.

Then the cycle turns.

Small caps begin to correct. The portfolio that looked exceptional six months ago now looks alarming. The investor stops SIPs, considers redeeming, and waits for "things to settle." The picture never feels clear enough to re-enter. By the time confidence returns, large caps have already recovered. The investor missed it.

This is the pattern. It repeats with small caps, with gold, with international funds, with sectoral themes — across every market cycle. The specific category changes. The underlying behaviour does not.

The tragedy is not that investors lose money in a single bad call. The tragedy is that they remain perpetually busy — switching, redeeming, reallocating, researching — while very little long-term compounding actually happens.

Why Most Investors Ask the Wrong Question First

When people think about investing, the conversation almost always begins with the same questions:

Which mutual fund should I buy?

Which sector is going to outperform this year?

Should I be in large caps or small caps right now?

Is gold a good buy at this price?

Should I wait for the market to fall before investing more?

None of these are bad questions. But they all share a common blind spot: they assume that the most important decision in investing is what to buy.

In reality, the more important question comes before any of that: How should the overall portfolio be structured?

That means deciding:

How much of your money should be exposed to equity markets

How much should sit in debt instruments

How much in gold or other protective assets

How much should remain liquid and accessible

How much risk you can genuinely absorb — not in theory, but in practice, when your portfolio is falling and every instinct tells you to act

These structural decisions are what determine how your portfolio actually behaves over time — how much it grows, how much it falls, how quickly it recovers, and most importantly, how you feel while all of this is happening.

That last part matters more than most people expect.

A Portfolio Is Not a Collection of Products. It Is a Combination of Exposures.

Think of it this way. Imagine two investors, each holding the exact same small cap fund — a good one, managed well, with a strong track record.

Investor A has allocated 80% of their wealth to this fund. They chose it because they believe in the story, they have done their research, and the returns have been compelling.

Investor B holds the same fund, but it represents only 20% of their portfolio. The rest is spread across large cap equity, debt, gold, and some liquid assets.

Here is how the same market events play out differently for each of them:

When markets rise, Investor A's portfolio looks brilliant. Investor B's looks comparatively ordinary — diversification is, by design, a drag when one category is running hot.

But when small caps correct — and they will, eventually — the experience is completely different:

Investor A (80% Small Cap) | Investor B (Diversified) | |

Portfolio fall during correction | 45–55% | 20–25% |

Emotional experience | Severe stress | Uncomfortable but manageable |

Likely behaviour | Stops SIPs, considers exit | Continues SIPs |

Recovery captured | Partial or none | Full |

Long-term outcome | Poor, despite good fund | Good, despite same fund |

The fund was identical in both cases. The outcome was not. The difference was entirely structural.

The Real Risk in Investing Is Not Volatility. It Is Behaviour.

Most people understand risk as the probability that something falls in value. A volatile investment is risky; a stable one is safe. This is intuitive — and not entirely wrong.

But it is incomplete in one critical way.

The deeper risk in investing is not that your portfolio moves. It is that you move — emotionally, impulsively, at exactly the wrong moment.

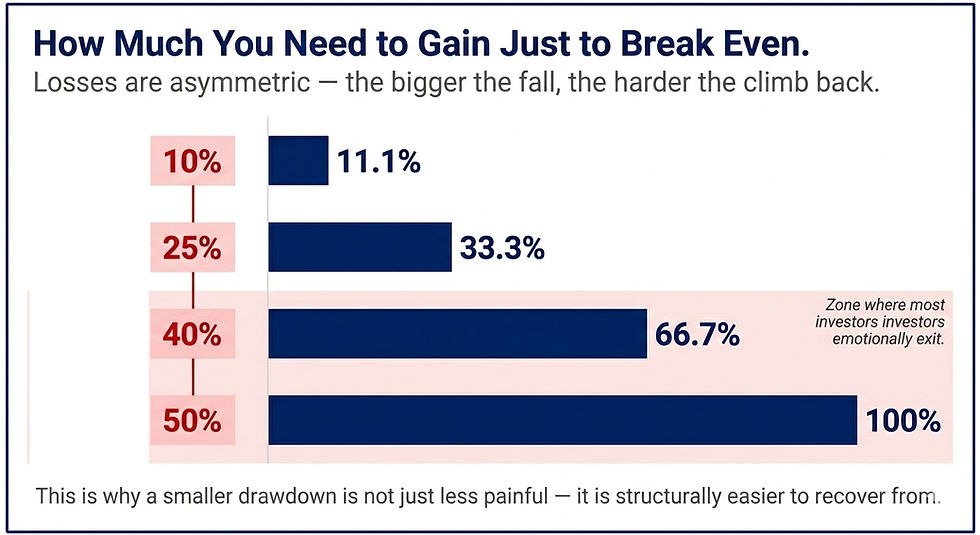

Here is why this matters mathematically:

The progression here is not linear — it curves sharply. And this is exactly where the emotional breaking point tends to occur. A portfolio falling 10% feels uncomfortable. One falling 20% creates genuine anxiety. One falling 40% or more has the power to completely change how a person thinks about investing — sometimes for years.

At those levels, investors tend to:

Stop SIP contributions ("Why keep investing if it keeps falling?")

Shift to cash or fixed deposits ("At least I won't lose more")

Avoid looking at their portfolio altogether

Exit after the fall has already happened

Delay re-entering because they fear another leg down

Each of these responses feels rational in the moment. None of them are good for long-term outcomes.

This is why asset allocation is, at its core, about behaviour management — not just mathematics.

A well-diversified portfolio does not prevent markets from falling. But it can reduce the severity of the fall to a level where you can actually hold through it. And holding through it is the entire game.

What Each Part of Your Portfolio Is Actually For

One of the most persistent mistakes investors make is judging every component of a portfolio through a single lens: return.

If one investment is earning 14% and another is earning 7%, the 7% looks like the obvious loser. If something has been flat for two years while markets have run up, it looks like dead weight. If a portion of capital is sitting liquid and accessible, it feels unproductive.

But this comparison assumes that every rupee in your portfolio is trying to do the same job.

It is not.

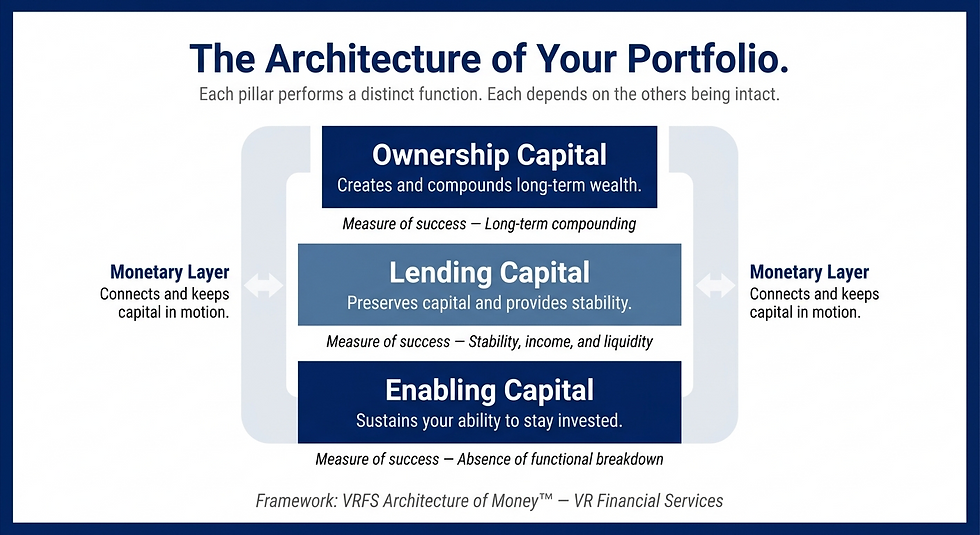

A useful way to think about this comes from a framework called the VRFS Architecture of Money™, developed inhouse and proprietory. Rather than classifying wealth by the products you hold, it classifies capital by the economic function each part is performing. It proposes that every rupee an investor deploys exists in one of four distinct states — each with a different purpose, a different measure of success, and a different role in keeping the overall structure alive.

Understanding these four states does not require deep technical knowledge. It requires a shift in the question you ask about your portfolio — from "what is this returning?" to "what is this supposed to be doing?"

Ownership — The Part That Creates

The first pillar is Ownership Capital. This is the portion of your portfolio that participates in productive or scarce assets — capital that holds a residual claim on the growth of something, whether that is a business, a piece of land, or any asset whose value is driven by productivity or scarcity.

The defining characteristic of Ownership is that its return is variable, uncapped, and never contractually guaranteed. You do not lend this capital to someone. You stake it. If the underlying asset creates value, you participate in that creation. If it does not, you bear the loss. There is no floor, no promise, no obligation from the other side.

This sounds risky — and in the short term, it is. Ownership positions can and do fall significantly during corrections. They can take years to recover. They require patience and the willingness to hold through discomfort.

But Ownership is the only part of a portfolio that can genuinely compound wealth over long periods. Because the return is residual and uncapped, there is no ceiling on what it can ultimately deliver. This is the creative pillar — the part of the portfolio where wealth is actually built, not merely preserved.

The practical implication: Ownership capital should be funded from surplus — money you genuinely do not need for any near-term purpose. It is long-term in nature, sometimes perpetual. Measuring it over one or two years, or comparing it against a contractual instrument, is a category error.

Its success is measured not by how much it returned last quarter, but by whether it is compounding meaningfully over a decade or more.

Lending — The Part That Preserves

The second pillar is Lending Capital. This is the portion of your portfolio where you act not as an owner, but as a creditor — extending capital to a borrower in exchange for a pre-defined, contractual return and the obligation of repayment.

The return here is not residual or variable. It is fixed, obligation-based, and defined in advance. You know what you will earn. You know when you will be repaid. The counterparty has a legal obligation to honour both.

This certainty is precisely what makes Lending Capital valuable — not because certainty is exciting, but because it is stabilising. It trades growth potential for predictability, and within a portfolio, that trade is worth far more than most investors recognise.

Lending Capital serves several functions that are easy to undervalue until they are needed:

It cushions the portfolio during equity corrections — when Ownership positions are falling, Lending capital tends to hold steady, reducing the severity of the overall experience

It provides accessible liquidity without requiring the sale of growth assets at depressed prices

It anchors near-term goals — any financial objective within the next one to three years has no business being exposed to the variability of Ownership; it belongs in Lending

It funds rebalancing — when Ownership falls and creates an opportunity, Lending is often the source from which you move capital back into growth without needing to bring in fresh money

The mistake most investors make with Lending Capital is judging it the way they judge Ownership. Asking why a debt fund is not performing like an equity fund is like asking why a seatbelt is not helping you drive faster. That is not its job. Its job is to be there — intact, stable, and accessible — precisely when Ownership is under stress.

Lending Capital does not create wealth. It protects the conditions under which wealth creation can continue.

Enabling Capital — The Part That Keeps You in the Game

The third pillar is the one most investors have never consciously thought about — and yet it is the one whose failure causes the most damage.

Enabling Capital is the portion of your wealth deployed to sustain your ability to remain a functioning investor. It is not there to grow. It is not there to earn contractual income. Its sole purpose is continuity — ensuring that you, as an investor, remain capable of staying in the wealth-creation process across time, stress, and real-life disruption.

Think of it this way: your portfolio can be perfectly structured, with excellent Ownership and Lending positions. But if a medical emergency wipes out your savings, if the loss of income forces you to liquidate equity at the bottom of a correction, if a lack of protection exposes your family to financial catastrophe — the rest of the architecture collapses. The investments survive on paper. The investor does not.

Enabling Capital prevents that collapse.

Its measure of success is unlike any other part of the portfolio. It does not aim to maximise return. It does not aim to minimise risk in the conventional sense. It aims to prevent functional breakdown — to ensure that survival, protection, operational capacity, and the ability to hold long-term positions are never compromised by real-world disruption.

This is why the Architecture of Money describes Enabling Capital as structurally subordinate but operationally primary. It must be in place before the other pillars can be confidently built. Ownership capital held without adequate Enabling underneath it is fragile — it exists in theory, but the investor's ability to sustain it through real market cycles is unreliable.

Some important characteristics of Enabling Capital:

Its return is indirect and functional — the benefit is your continued ability to earn, decide, and hold positions, not a number on a statement

Its risk runs in both directions — too little causes functional breakdown; too much wastes capital that should be compounding in Ownership or Lending

It is not a residual category — capital parked here because it has no other home is misallocated, not Enabled

The practical question Enabling Capital answers is this: if markets were inaccessible for twelve months, could you survive, continue operating, and hold your investment positions without being forced to liquidate? If the answer is no, the architecture is incomplete — regardless of how good the Ownership and Lending positions look.

The Monetary Layer — The Part That Connects

The Monetary Layer is not a pillar of wealth creation. It is the connective infrastructure — the medium through which capital moves between Ownership, Lending, and Enabling functions.

This includes non-yielding cash, current account balances, and liquid holdings held purely for settlement, timing, and contingency. It does not generate return. It does not preserve capital through contractual income. It exists for one purpose: to keep the rest of the architecture responsive, liquid, and in motion.

Without it, the system seizes. Capital cannot move from Ownership back into Lending when rebalancing is needed. It cannot fund Enabling requirements without forcing an untimely liquidation of growth positions. The Monetary Layer is what gives the investor control over timing — the ability to act when an opportunity arises, respond when an emergency hits, and move capital deliberately rather than reactively.

One distinction worth drawing clearly: not everything liquid is the Monetary Layer. Once a liquid holding begins earning contractual interest — a liquid mutual fund, a short-term deposit — it has crossed into Lending. The Monetary Layer is strictly non-yielding. The line between the two is the presence or absence of contractual return.

The discipline around the Monetary Layer runs in both directions:

Too little — and the portfolio loses responsiveness; emergencies force liquidation of Ownership at the worst moments

Too much — and capital sits idle, eroded by inflation, compounding nothing; the Architecture of Money is clear that excess non-yielding liquidity beyond genuine functional need is a governance failure, not prudence

The goal is not to maximise cash. It is to hold enough that the rest of the portfolio is never forced to act from desperation — and not so much that the habit of holding cash crowds out the discipline of deployment.

Why All Four Need Each Other

Each pillar on its own is incomplete. A portfolio that is entirely Ownership — all growth, no preservation, no protection — may compound impressively during good years. But it has no cushion when markets fall, no liquidity when life demands it, and no structural buffer that allows the investor to hold through the inevitable correction without panicking. The investor who is overwhelmingly concentrated in growth assets during a bull market feels invincible. During a sharp, extended drawdown, that same investor is usually the one who exits at exactly the wrong time, locks in the loss, and misses the recovery.

A portfolio that is entirely Lending — all preservation, no creation — is stable in the short term but quietly losing ground to inflation over decades. Safety without growth is stagnation.

Ownership without adequate Enabling underneath it is fragile leverage — positions that look strong on paper but cannot be held through real-world disruption. And a Monetary Layer held in excess, without deliberate deployment into the three pillars, is capital that is neither creating, preserving, nor enabling anything.

Each part needs the others. The proportions will differ from investor to investor, depending on goals, time horizon, income stability, and genuine behavioural tolerance for volatility. But the principle is consistent: a resilient portfolio is not the one with the highest-returning component. It is the one where each component is performing its designated function, and those functions hold together across market cycles.

Rebalancing — Keeping the Architecture Honest

Even a well-designed portfolio will drift over time. When Ownership has had a strong run, it quietly becomes a larger share of the total than originally intended. A portfolio that started with a considered balance across the pillars may find itself heavily skewed toward Ownership after a bull market — not because of any deliberate decision, but simply because those positions grew faster than everything else.

This sounds like a good problem. In one sense it is. But the consequence is that the portfolio is now carrying more Ownership risk than its Lending and Enabling pillars were designed to support. The structure has become more aggressive than the investor chose it to be — silently, without a single conscious decision.

Rebalancing means periodically returning the portfolio to its original structure. In practice, this involves:

Reducing exposure to what has grown significantly

Adding to areas that have temporarily underperformed

Keeping risk at the level you originally chose

Preventing dangerous concentration from building up silently

This feels uncomfortable. Nobody likes selling winners. Nobody likes adding to categories that have recently disappointed. But that discomfort is precisely why rebalancing works — it creates mechanical discipline in a process that would otherwise be driven entirely by emotion.

Over long periods, disciplined rebalancing is often one of the biggest contributors to stable, sustainable portfolio outcomes.

Investors who rebalance consistently tend to experience smaller drawdowns, maintain the structural integrity of their portfolio through corrections, and compound more steadily over long periods than those who let their architecture drift unmanaged.

Structure Before Selection

The point of this entire section is not to introduce a framework for its own sake. It is to shift the sequence in which most investors make decisions.

Most investors begin with product selection — which fund, which category, which asset class looks best right now. The Architecture of Money suggests that this is the second decision, not the first. The first decision is structural: what function does this capital need to perform, and which pillar does it belong in?

When that question comes first, product selection becomes considerably clearer. You are no longer comparing every investment against every other investment on a single return axis. You are asking whether each investment is doing its designated job well — and whether the overall structure holds together.

That shift — from product-first to function-first thinking — is what separates portfolios that are built to be held from portfolios that are built to look good until the next correction arrives.

Why Chasing Last Year's Winner Is a Losing Strategy

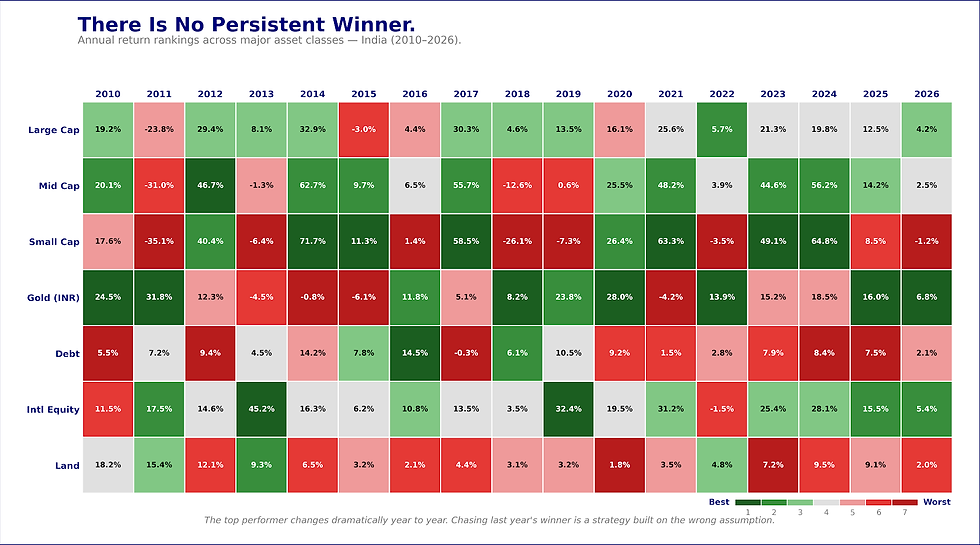

One of the hardest things to accept about markets is that performance leadership rotates — constantly, unpredictably, and often in ways that confound expectations.

There are years when large caps significantly outperform small caps. There are years when the reverse is true. There are extended periods when gold outperforms equity. There are years when international markets beat domestic ones handily, and years when the opposite is true.

This is not a bug in markets. It is a feature. Different asset classes respond to different economic conditions, and those conditions are always changing.

But investor attention — and investor money — tends to chase the recent leader anyway. The reasons are understandable. When your colleague's small cap fund is up 60% and yours is up 18%, it is genuinely difficult to hold conviction about diversification. The temptation to reallocate is real.

The problem is that by the time most investors act on this impulse, the cycle is often already turning. They enter toward the end of the outperforming category's run, experience the correction that follows, and exit having bought high and sold low. Then they repeat the same process with whatever the next exciting category happens to be.

The solution is not to predict which category will win next. Nobody can do that reliably. The solution is to hold a structure that participates in whichever category leads — because you are in all of them — without being devastated when any single one underperforms.

Investing Is About Preparation, Not Prediction

Most investors want certainty. They want to know which fund will perform best, which sector will lead next year, whether now is a good time to invest or whether they should wait. The search for that certainty drives an enormous amount of activity — reading reports, watching news, listening to experts, switching products — most of which ultimately does very little to improve outcomes.

Markets do not reward certainty. They reward preparation.

The difference matters:

Certainty-Seeking | Preparation-Based |

Trying to pick this year's best category | Holding a structure that covers multiple categories |

Waiting for the "right time" to invest | Staying invested through multiple cycles |

Reacting to corrections with exits | Using corrections to rebalance |

Judging the portfolio by last year's returns | Judging by whether goals are on track |

Constantly switching | Periodically reviewing and rebalancing |

A prepared portfolio has growth assets, defensive assets, liquidity, and the structural resilience to survive multiple market environments. It does not need perfect decisions at every turn. It just needs to keep running — through the bad years and the good ones alike.

That is the real purpose of asset allocation. Not to win every year. Not to hold the best-performing category at every moment. But to build something sturdy enough to survive when things go wrong, and sustainable enough to compound meaningfully across the decades when things go right.

Framework reference: The capital function lens used throughout this section draws from the VRFS Architecture of Money, a proprietary structural framework developed by Rajeev Roshan R, Principal and Founder of VR Financial Services.

This is Part 1 of a three-part series on Asset Allocation.

VR Financial Services

Empowered Wealth. Personalised Journey. Tech-Enabled Precision.

VR Financial Services, based in Bengaluru and founded in 2019, is a founder-led financial distribution firm. We help individuals, families, businesses, and trusts access financial products and build structured portfolios with greater clarity, discipline, and convenience.

What We Offer

End-to-end access to financial products across mutual funds, NPS, fixed deposits, bonds, insurance, and more

Seamless digital execution with consolidated portfolio tracking and reporting

Research-backed insights, portfolio monitoring tools, and performance reporting

Life and general insurance solutions to support protection needs across different life stages

Liquidity support options, including loans against mutual funds and other eligible assets

Our Approach

We go beyond product access by helping clients build structured financial systems that can adapt over time.

Our approach is:

Structured and goal-oriented, so portfolios can evolve with changing life stages and market cycles

Built around Core + Satellite frameworks that support both stability and flexibility within portfolios

Transparent and technology-enabled, making execution, tracking, and monitoring more efficient

Focused on disciplined allocation, long-term thinking, and consistent portfolio management rather than short-term market movements

At VR Financial Services, we believe wealth is not built by reacting to every market movement, but by having the right structure, product mix, and execution framework in place over time. Our role is to help clients stay prepared, stay invested, and stay aligned to their financial objectives.

Empowered Wealth. Personalised Journey. Tech-Enabled Precision.

🔗 LinkedIn – VR Financial Services

Disclaimer:

Mutual Fund investments are subject to market risks. Please read all scheme-related documents carefully before investing. The information shared by VR Financial Services is for educational and informational purposes only and should not be considered a recommendation or an offer to buy or sell any financial product. Past performance is not indicative of future results. Investors must ensure KYC compliance through authorised intermediaries, conduct their own due diligence, and make informed decisions. VR Financial Services does not guarantee returns or offer fixed/assured return schemes—any such claims are misleading and prohibited by SEBI. All investment transactions must be carried out only through official channels, and investors should never share personal credentials or OTPs. We do not solicit funds or commitments via social media, which is used strictly for investor awareness and education.